Don't Stick Your Head In The Sand

With so many mortgage holders still rolling off fixed interest this year, we think it is most important to keep drumming this message.

It is highly likely that you or someone close to you will be screaming HELP this year when their existing very low fixed interest rate (could be in the low 2% range) rolls over to whatever the then current standard variable rate (could be 6% or higher if it is later in the year).

With the expectation that interest rates will keep rising for a few more months yet1, perhaps peaking in May, there are good reasons to be paying attention to your spending and time to consider how you are going to pay your higher mortgage repayments.

One reason we think that people may not be paying attention is that those still on low interest rates and subsequently lower mortgage repayments are continuing to live life as though nothing has changed… spending money on:

- Outings

- Dinners

- Parties

- Movies

- Clothes

- Furniture

- Renovations

- Cars…

The list could certainly go on.

And let’s not forget about travel!

There have never been so many people lining up at airports ready to fly to that long awaited holiday destination. In November last year, overseas departures increased by 162,610 trips to a total of nearly 1.2 million people traveling that month2.

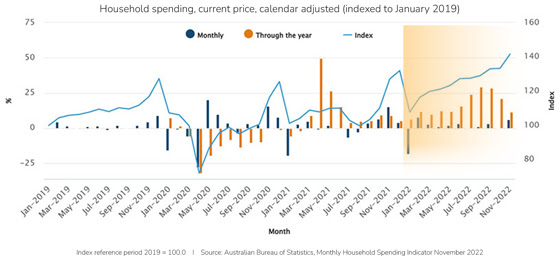

And when you look at the chart below you can see how housing spending increased from January 2022 to November – at the same time as interest rates were rapidly hiking. Household spending increased 11.4% and spending on services 17.1%.

What can you do if your mortgage repayments double or triple this year?

Well, the first thing is to take action well before it happens. The end of the year will approach us like a lightning bolt so please let’s all take our heads out of the sand and take responsibility for our spending. This alone can contribute to reducing rising inflation and perhaps put a halt to the ongoing interest rate rises.

Why are our spending habits important?

Because your spending habits are directly related to how much you can borrow and whether you will be able to refinance or not.

If you are on a fixed interest rate, the first thing you should do is find out your expiry date. Then seek guidance from us, as your finance specialist, as soon as you possibly can to schedule a time in our diary.

We are usually in a better position than your lender to help you manage the transition when your fixed term loan expires as we have access to a range of finance products and understand the current incentives designed to motivate you to switch lenders.

How to negotiate a better deal when your fixed term expires

It is best to contact us at least three months before your fixed loan expires or as soon as you have read this article!

Here are some options we may discuss when your fixed term expires:

- Do nothing! Determine if you should continue with the variable rate loan on offer from your existing lender.

- Fix your loan for another fixed term period.

- Refinance your loan with another lender if there are more appropriate outcomes than staying.

- Split your loan (between fixed and variable) with your existing or new lender.

As your mortgage specialist, we can complete an interest rate check for you and help you compare other options available with the same lender, or we can explore potential refinancing options with competitive lenders’ rates.

The different possibilities highlight that there is no one-size-fits-all approach for homeowners nearing the end of a fixed term. It is worth knowing the advantages and disadvantages of each option:

Option – do nothing

Stay with the variable rate on your current loan

This ‘do nothing’ option means staying with the same lender and having your loan revert to the standard variable rate once the fixed term expires.

This may be the easy option, however it is also most likely going to be the most expensive.

It could however, also be your ONLY option.

You may have been initially enticed to take up your loan with an introductory ‘special rate’ from your lender. However, interest rates have increased nine times over the last 12 months so you would be wise to seek guidance from your mortgage specialist about offers from other lenders that may be more competitive.

In the current environment of rising interest rates, to survive the interest rate increases it is wise to start planning and budgeting for higher monthly repayments well beforehand while investigating other rates available in the market.

Should you have a packaged loan that includes a number of benefits and savings that make sense, then you might opt to stay with your current lender.

You may want to be loyal to your lender, but chances are your lender won’t reward your loyalty with its market-leading rate. This rate is usually given to NEW customers.

When lenders offer preferential rates to new customers over existing customers, it is called the ‘loyalty tax’.

Remember, we can help you manage your existing lender and explore more competitive options.

Option – re-fix

Take out another fixed interest loan

If you want certainty about your monthly repayments and do not want to worry about interest rates rising, then you may consider locking in another fixed term for several years.

But the days of very low fixed rates are probably over and you will need to see what competitive deals may still be available.

While locking in another fixed term will protect you from any further interest rate rises, it can leave you ‘high and dry’ if interest rates happen to fall over the duration of your loan.

Fixed Interest loans are generally less flexible than other loans that can offer features such as offset accounts, redraw facilities and fee free extra payments.

In addition, should you need to cancel your fixed loan for any reason, such as selling or refinancing your home, or simply looking for a better rate, then you will be charged break costs which can be significant.

Always seek our guidance before locking in another fixed term.

Option – refinance

Refinancing your loan with another lender

Well before your fixed rate loan expires, we offer a loan health check to compare yours with other lenders in the wider market.

Our role is to help you find a finance offer or present the advantages and disadvantages of cashback incentives. Our main focus is that if refinancing, you recover the costs.

It may not actually make good financial sense to accept a higher interest rate just to take advantage of the cashback.

Many lenders are making competitive offers to attract new customers. These may or may not end up being a true saving.

Other factors to be aware of are changes to your personal circumstances from the time you first took out your fixed interest loan. Changes to your circumstances may affect the amount you can borrow.

For example:

Increasing your credit card limit, having a car loan or even having a child can significantly decrease the amount you are able to borrow.

Of course, if you happen to be earning more than previously, then this may increase your borrowing capacity. The only way to know for sure is to talk to us.

The best interest rate deals usually apply to borrowers who have between 20% to 40% equity in their homes. In other words, they only need to borrow between 60% and 80% of the value of their home.

If you have less than 20% equity, you will most likely have to pay lenders’ mortgage insurance (LMI) which can be a significant cost that offsets any potential savings you could have made.

Refinancing to a lower rate may suit those who have equity in their homes and meet their lender’s other serviceability requirements. However, it will most likely come with other costs and fees.

Option – have your cake and eat it too!

Split your loan between fixed and variable

Did you know it is possible to have a combination of a fixed rate and a variable rate loan?

Most lenders who offer this type of loan will allow you to choose the proportions of each. For example, you may opt for 40% fixed and 60% variable.

Splitting the loan provides repayment certainty for the fixed component while allowing some flexibility with the variable portion.

If variable rates rise, the fixed portion of your loan will be unaffected. But if rates fall, the fixed portion will cost you more than the variable and this will offset any savings you were relying on.

Split loans are not always an option on every available loan so your choice of loans or lenders may be limited.

If you are undecided on whether to fix or refinance your loan or you are looking for a combination of flexibility and certainty, then splitting your loan may be an option for you.

Will you be a ‘mortgage prisoner’?

You also need to be aware that you may not be able to refinance or change lenders either. Not all mortgage holders will have the capacity to move to another lender. So you may have to stay put for a while. DO NOT RISK YOUR CREDIT SCORE by shopping around. Allow us to do the research on your finance options. If we can help you find an appropriate and alternate solution, then we will. However, if it is best for you to stay where you are for now, we will tell you that too!

As always, please discuss all your options with us. We are specialists in the industry and are here to help you with these decisions, AND it may be the largest decision you need to make this year. So don’t do it alone.

With your best interest always in mind…

We look forward to hearing from you.

Regards,

Rukmal (Rocky) Wijesooriya

Note:

Our experience and professional services are governed by high standards inclusive of privacy provisions together with a well-established complaints process. We are governed and registered by ASIC, AFCA and FBAA for your protection of dealing with us.

— March RBA Update —

There are no surprises with another rate rise expected today.

Moving another 25 basis points this month the official cash rate is now 3.6%

All four majors now forecast average interest rates to be 6.63% this month.

The only good news in sight is that 2 of the majors are predicting the cash rate to peak in May at 4.10%.

But with all predictions, we wait with bated breath…

While some may be struggling with mortgage repayments, many are taking the opportunity to snap up some good investment property deals.

With increased equity, rising rentals, a shortage of rental properties and recent wage growth, NOW might be a great time to consider expanding your property portfolio. If this sounds like you, then let’s chat.

02 9499 5697

Use this link to book a call/ zoom meeting: https://calendly.com/rukmal/

Intelligent Accounts and Finance

45A Spencer Road

Killara NSW 2071

02 9499 5697

0423547547

rukmal@

intelligentaccountsandfinance.

Australian Credit Licence: : 412778

Credit Representative Number: : 534206

ACN : 148919715

Disclaimer: This article provides general information only and has been prepared without taking into account your objectives, financial situation or needs. We recommend that you consider whether it is appropriate for your circumstances. Your full financial situation will need to be reviewed prior to acceptance of any offer or product. It does not constitute legal, tax or financial advice and you should always seek professional advice in relation to your individual circumstances.